A Written Information Security Plan As An Important Tool for HR and Benefits Administration

The IRS recently highlighted the importance of maintaining a Written Information Security Plan to protect sensitive HR and benefits data from cyber threats.

Questions about your benefits? Contact your HR administrator.

A mid-year ACA checkup helps ensure that your organization is on track to meet employer mandate requirements, avoid penalties, and simplify year-end reporting.

As we reach the midpoint of the year, it’s the ideal time for HR teams to revisit Affordable Care Act (ACA) compliance responsibilities. A mid-year checkup helps ensure that your organization is on track to meet employer mandate requirements, avoid penalties, and simplify year-end reporting. This article provides a practical ACA compliance checklist tailored for Applicable Large Employers (ALEs).

If premium rates or employee wages have changed, recalculate affordability and adjust contributions if necessary.

Review Employee Classification and Tracking

For organizations with variable-hour or part-time workers, ensure you’re correctly using the look-back measurement method to determine full-time status. Validate that timekeeping and payroll systems accurately track hours and reflect proper employee classifications. Any misclassification could lead to offer failures and potential penalties.

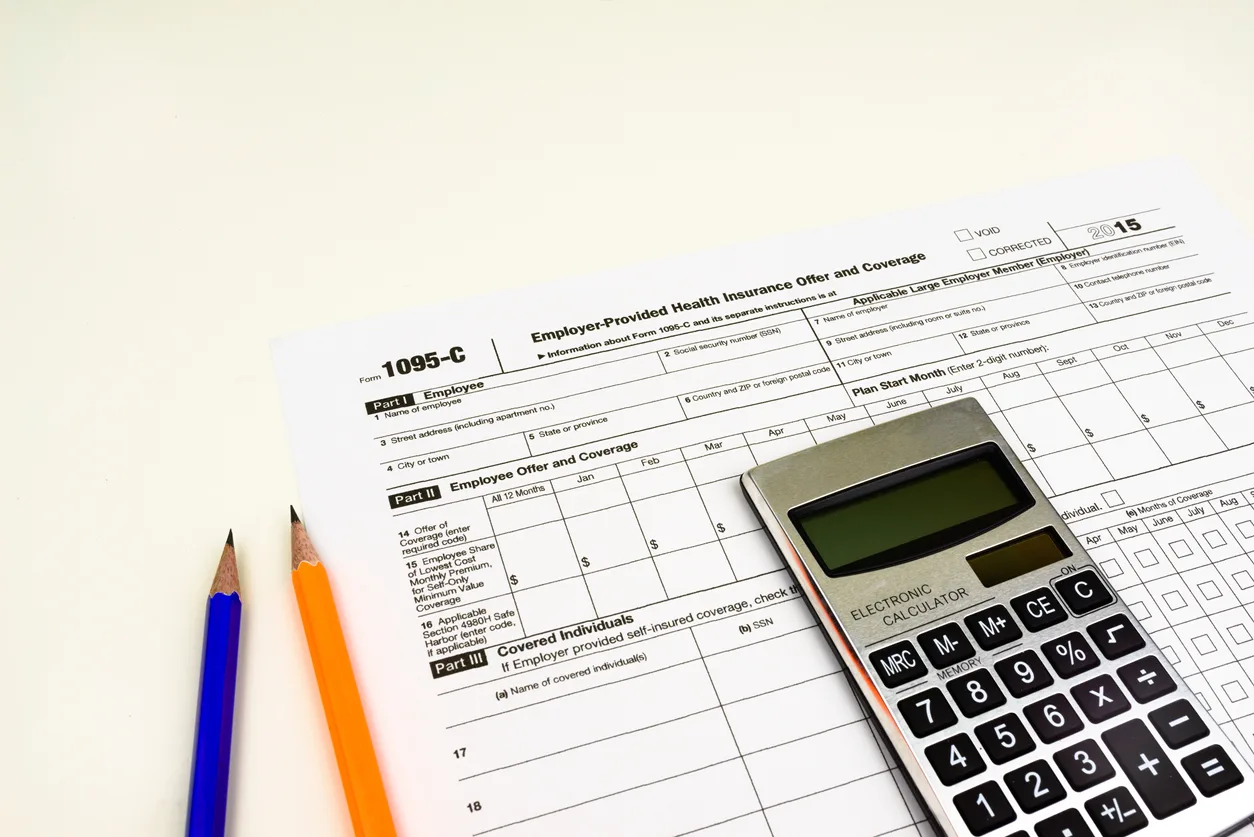

Prepare for Year-End Reporting

Although ACA reporting occurs early in the following year, now is the time to ensure your data is accurate and complete. Double-check that:

Early preparation helps avoid filing errors and reduces the burden on HR at year-end.

Monitor for IRS Notices

Keep an eye out for IRS Letters such as:

If you’ve received any notices, ensure you’ve responded appropriately and documented all communication. If no notices have been received, this is still a good time to confirm that prior reporting was complete and accurate.

Plan Ahead for Open Enrollment

If your organization plans to change health plan options or employee contributions during open enrollment, consider how those changes may impact ACA compliance. Ensure new plans still meet MEC, Minimum Value, and affordability standards. Document any updates early and plan employee communications accordingly.

Conducting a mid-year ACA compliance review helps your organization stay ahead of regulatory requirements, reduce penalty risks, and create a smoother experience during year-end reporting. HR professionals who approach compliance proactively are better positioned to support their organizations and employees year-round.

Benefit Allocation Systems (BAS) provides online solutions for: Employee Benefits Enrollment; COBRA; Flexible Spending Accounts (FSAs); Health Reimbursement Accounts (HRAs); Leave of Absence Premium Billing (LOA); Affordable Care Act Record Keeping, Compliance & IRS Reporting (ACA); Group Insurance Premium Billing; Property & Casualty Premium Billing; and Payroll Integration.

MyEnroll360 integrates with major insurance carriers for enrollment eligibility management (e.g., Blue Cross, Blue Shield, Aetna, United Health Care, Kaiser, CIGNA and others), and with leading payroll platforms for enrollment deduction management (e.g., Workday, ADP, Paylocity, PayCor, UKG, and others).

This article is for informational purposes only and is not intended as legal, tax, or benefits advice. Readers should not rely on this information for taking (or not taking) any action relating to employment, compliance, or benefits. Always consult with a qualified professional before making decisions based on this content.

The IRS recently highlighted the importance of maintaining a Written Information Security Plan to protect sensitive HR and benefits data from cyber threats.

Educational assistance programs let employers help pay employees' tuition and student loan expenses tax-free, and new IRS guidance clarifies how they work.

Most ACA penalties stem from operational issues that occur throughout the year, not just year-end reporting.